Updated Sep. 22, 2019. Originally published Jun. 25, 2013.

If you’re just stumbling across this, please click here for the other posts in the series.

Budgeting

For some, budgeting is a scary word. It doesn’t need to be, though. Budgeting is simply making a plan for which of your income will go to what uses. Some of you may be responsible for your overall household budget. But even those of us who aren’t have something we need to budget. (Unless you never use any money. If someone else in your household does all the bill-paying and shopping, you may be the rare exception.)

If you are responsible for the full household budget, you’ll have a lot more planning/setting up to do with your budget. If you aren’t, you’ll have less — but you will probably still need to meet with whomever does (probably your husbands, for most of you) to sort out how much you need for the expenses you are responsible for. (For me, that’s anything that’s bought for the home on a regular basis – like groceries, clothing, paper goods, etc.)

Determining the Budget

STEP 1: Make a note of your income, and of all of your non-negotiable expenses.

(By non-negotiable, I mean not only that it’s not negotiable that it is an expense, but also that the cost is predetermined. You can’t decide, for instance, how much your rent or mortgage is. And you may be able to affect your electric or water bill a little, but you can’t just decide on an amount and choose to work within that.)

If you are not the primary budgeter in your home, you can skip step 1.

STEP 2: List all of your other (more negotiable) expenses.

If you are not the primary budgeter in your home, this task will probably fall to someone else, but you will want to provide your input.

STEP 3: Determine how much is left of your income after your non-negotiable expenses are accounted for, and decide on how much to allocate for each of the expenses listed in step 2.

This is another step where you will probably want to work together with the primary budgeter for the household, even if that is not you. If you are purchasing the groceries, for instance, you may need to help someone who never shops for groceries know what is reasonable.

Personally, I find this part very tricky. How do you know if you need to budget more for food or just do a better job of shopping? How do you determine whether it’s reasonable or indulgent to allocate more for clothing? Ultimately, questions like these all require judgment calls, and the answers will vary based on your family size, location, and other circumstantial factors.

But if you’re starting from scratch, you may need some guidelines. Just keep in mind that they’re exactly that – use them as a starting point, not as rule of law! I haven’t found many concrete guidelines, but I have seen it suggested that groceries approximate $100/month per family member (Some people are able to do even better. With the way prices have risen in recent years, though, this seems a fairly accurate estimate for those looking to feed their families good food. And by “good” I mean quality, not luxury.)

In other areas, I confess I am, myself, at something of a loss. It’s clear, for instance, that something needs to be allocated for clothing. The family can’t just go naked! But how much could have an extremely wide range of answers. Whether your kids can pass things down, how hard family members’ sizes are to locate, whether or not you sew any of your own clothing, and whether there are good secondhand stores in your area are all potential factors.

For some things, you may need to start with a baseline and multiply. Gifts, for example. Decide on an average per-recipient amount and multiply by the number of gifts you have to give throughout the year. Then you can adjust as necessary.

(If your budget needs a drastic overhaul, you may benefit from the debt reduction information coming up next month.)

STEP 4: When you have sorted out the whole plan, copy it neatly and choose a safe place to keep it (like in a “finances” section of your household notebook). Put it there!

Determining the Method

Creating the budget was only one necessary element. Working the budget is also essential. You will need to settle on the method you prefer for day-to-day spending within the budget.

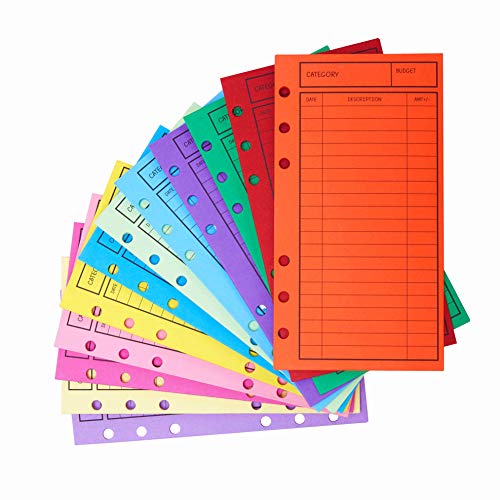

Lots of people swear by the cash envelope system. I appreciate the concept and used to use it (in fact, I even put together a tutorial for making a pretty envelope book), but in this internet age, I run into problems with it. What do I do if I make an online purchase? When I buy our vitamins and personal care products from Vitacost, if I’m using the cash envelope system, it makes a mess of things. It also confuses me if I’m buying items from multiple categories at once. (Heaven forbid we should buy clothes and food and school supplies in one Wal-Mart shopping trip!)

Clever Fox Cash Envelopes for Budget System 12 Pcs Budget Envelopes, Vertical LayoutAntner 12pcs Binder Pockets A6 Size 6-Hole

12 Pcs Budget Envelopes, Vertical LayoutAntner 12pcs Binder Pockets A6 Size 6-Hole

In recent months, I’ve seen variations on this method that I think would work better for us. There are, for instance, several different smartphone apps that are designed to be digital versions of the envelope system. You use your debit card to pay, but the apps enable you to divvy up the funds into the appropriate virtual “envelopes.” (See the “resources” list below for some options.) Mint.com is similar, too.

One of the most intriguing systems I’ve seen is Jordan’s system of 7 bank accounts. Yes, it sounds like a lot, but when you read about the system, they all make sense! (Capital One online, formerly INGdirect, makes tracking multiple accounts online super-easy. Their online banking layout is easier than any I’ve ever used.)

You may have another method that works for you, like an Excel spreadsheet. Unfortunately, because budgeting methods and materials will vary, I can’t really break this down for you, so we’re going to roll it all into one step:

STEP 5: Set up a system for working the budget, and start using it.

Resources:

- EEBA app (web, Android, iPhone)

- The Envelope System (iPhone app)

- Mint.com

- Capital One

- household budget spreadsheets

- Home Sweet Frugal’s post about her budget binder

- Dave Ramsey offers recommended percentages.

- Money Jars Method (or an ebook for more detail)

If you’re just stumbling across this, please click here for the other posts in the series.

[…] Now, we’re not talking about budgeting the funds for these; that should have been addressed last week. Rather, we’re talking about organizing the paperwork and the […]